APRES PIQUES ET REPLIQUES AU SOMMET DE L’ETAT, PLACE AU TRAVAIL , (Par Cheikh Tidiane SY Al Amine)

On May 29, 2026, former President of the Republic of Senegal, Abdoulaye Wade, entered the rare circle of centenarians. To mark the occasion, official tributes and documentaries abounded, recalling the life of a man who traversed a century of African history without ever faltering. Among all the maxims this brilliant lawyer bequeathed to his people, one resonates today with particular force: "ONE MUST WORK, WORK HARD, ALWAYS WORK," and now, above all, WORK WELL. This message is no longer merely a moral imperative. It has become a national imperative. For two years, from March 2024 until now, Senegal has lived to the rhythm of barbs and retorts, accusations and counter-accusations, audits and counter-audits. The political class has debated, torn itself apart, and reformed. Meanwhile, the figures continued their relentless decline. And what they say today is unambiguous: it's time to get to work.

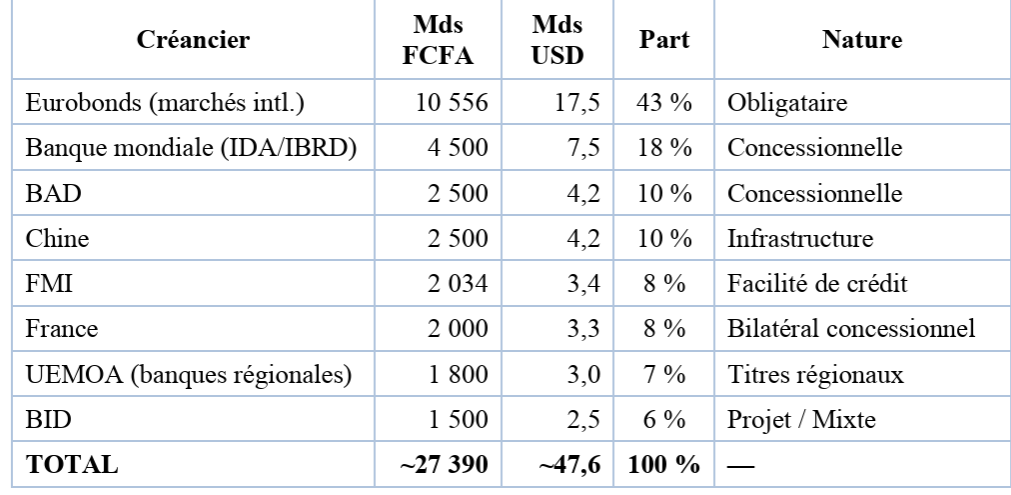

The anatomy of an out-of-control debt

To understand the scale of the challenge, we must first look at the figures. The structure of Senegal's debt reveals a profound imbalance, dominated by a particularly volatile creditor: the international bond markets.

Structure of Senegal's public debt by creditor

Sources: DGDP data, IMF, estimates. The most troubling lesson from this picture is this: nearly half of Senegal's debt is held in market instruments, Eurobonds, which are subject to the volatility of global interest rates, the whims of rating agencies, and the expectations of institutional investors. This is where systemic risk is concentrated.

Observation: Senegalese Eurobonds have lost value on the markets. The good news: Senegal met its first major deadline of March 2026, and the $488 million in bonds owed to external private creditors was honored. This rebound is real, but fragile. It rests on a signal of credibility, not yet on a structured program. The regional market is showing signs of saturation.

Reprofiling or restructuring: the smart way

Faced with this situation, two words dominate the debate: restructuring and reprofiling. They are not synonymous, and this distinction is fundamental for the country's future. Restructuring implies a haircut, a discount on the principal. This is the path taken by Ghana, which accepted a 37% haircut on its debt in 2023, at the cost of prolonged exclusion from international markets and severe weakening of the national banking sector. For Senegal, this would be a catastrophic choice: our regional banks (Ivorian, Senegalese, and Togolese) are themselves exposed to Senegalese sovereign debt. A haircut would destabilize the entire WAEMU region. Reprofiling, on the other hand, means extending maturities without a haircut, converting costly debt into concessional financing, and proactively managing repayment peaks. It allows for managing the critical maturities of 2026 and 2031 without inflicting losses on creditors. The combination of levers available over 2026–2027 makes it possible to free up budgetary margins of several billion dollars by combining new revenues, savings on spending and relief from post-reprofiling debt service.

Proposal for differentiated reprofiling by creditor

Eurobonds (43%, 17.5 billion USD)

This is where the effort is most urgent and visible. A liability management operation must be launched quickly to extend the maturities of the 2026, 2028, and 2031 bonds through a voluntary debt exchange. Investors would receive new 7–10 year instruments with a reasonable coupon premium in exchange for immediate debt service relief. A prerequisite is an agreement with the IMF: without this seal of institutional credibility, private investors will not trust the exchange. To date, the lack of IMF program approval limits the signal the country can send to the markets.

World Bank and AfDB (28%, USD 11.7 billion)

These multilateral creditors are the most flexible on terms and the most responsive to sustainable development arguments. Three levers must be activated: (1) the partial rescheduling of principal repayments over an additional 5 to 7 years; (2) the conversion of a portion of the debt into climate finance (debt-for-nature swaps, RSF instruments); (3) additional financing of strategic projects in oil, gas, and agribusiness within the framework of the PRES.

China (10%, USD 4.2 billion), France (8%, USD 3.3 billion), and others: Chinese debt is primarily tied to specific infrastructure projects. Negotiations should focus on extending grace periods from 3 to 5 years and renegotiating interest rates within the framework of a structured bilateral dialogue. Beijing has agreed to debt rescheduling in other African countries; Senegal can formalize this request within the G20 and Common Framework. This is also an opportunity to revitalize historical relationships with France and other bilateral partners for budget support and, potentially, debt forgiveness in the form of grants. Indeed, Senegal has benefited from this under the HIPC initiative or through bilateral debt cancellation, as was the case in 2005 with Norway. The WAEMU regional market (7%, USD 3 billion): Regional banks are both creditors and systemic partners. Orderly debt management preserves their balance sheet. The solution is a coordinated bond issuance program on the WAEMU market with longer maturities (5 to 7 years), supported by clear communication on the budgetary trajectory. The IMF equation: negotiate firmly on the three points of contention. The cornerstone of this entire system remains the agreement with the IMF. A mission is scheduled for June 15, and an agreement would lend credibility and facilitate access to concessional financing. But three points of contention must be negotiated skillfully. 1. Eliminating Fuel Subsidies: Morgan Stanley and Barclays believe the IMF will not approve an agreement without the elimination of fuel subsidies, a measure described as politically and socially risky given that the energy bill could exceed $2 billion in 2026. Senegal's position must be clear: yes to rationalization, but over a 24- to 36-month period, supported by a targeted social transfer program for vulnerable households. Abrupt elimination would be socially explosive in a context of high unemployment. We are not asking to forgo reform; we are asking that it be implemented without triggering a social crisis that the IMF itself will have to manage. 2. Revising Growth Outlooks: Real GDP growth is projected at around 5% for 2026 (driven by oil and gas), compared to a forecast of 7.8% in 2025. However, the IMF has raised concerns about the fiscal assumptions, considering the assumed "very high tax yield" to be a significant risk. Senegal must agree to revise its revenue assumptions downward for 2026–2027, while vigorously defending its real growth prospects, among the highest in sub-Saharan Africa. Growth fueled by energy, gold, and agribusiness is the strongest argument for convincing creditors that the debt is ultimately repayable. 3. The PRES (Economic and Social Recovery Program): The recycling of public assets without transfer of ownership, estimated at 1,091 billion over four years within the framework of the overall PRES, represents an underestimated lever. The government must present to the IMF a vision for the Economic and Social Recovery Plan (PRES) that is not merely a communication document, but a structured, costed program that can be reviewed annually. This is the difference between a country that manages its debt and one that is burdened by it. Reviving investment: the other side of the coin. Debt restructuring only makes sense if it frees up resources for productive investment. The strategy to follow consists of: gradually consolidating public finances by reducing central government operating expenses; preserving public investment; reviving private investment; and developing specific measures to stimulate economic growth. Senegal has real assets: growth boosted by gas, oil, and gold; an agricultural sector capable of absorbing hundreds of thousands of jobs; and a private sector awaiting clear signals. A constantly improving tax administration forms the basis for a credible rebound. But these foundations are useless if budgetary resources are entirely absorbed by debt servicing. This is why restructuring is not a concession to weakness, but a strategic act in service of growth and employment. Conclusion: Standing up to negotiate. As Senegal celebrates the centenary of Abdoulaye Wade's birth, it would be tempting to limit ourselves to tributes and commemorations. But the true way to honor this man, this tireless builder, is to tackle head-on the challenges his country faces. The last two years have been marked by political battles, audit revelations, institutional tensions, ousters, and checks and balances. All of this was perhaps inevitable in a democracy seeking to rebuild itself on more transparent foundations. But the time for barbs is over. Numbers have no political affiliation. Therefore, our leaders—President Faye, the former and current Prime Ministers, the Minister of Finance, and the negotiators with the IMF—must heed the centennial call not as a mere ritualistic formula, but as an operational roadmap: We must work. Work harder. And keep working. We must work to convince creditors that restructuring is in their interest as much as it is in ours. We must work to negotiate with the IMF not as supplicating supplicants, but as sovereign partners with a coherent plan. We must work to build social transfers that will allow us to adjust subsidies without abandoning the most vulnerable. We must work to invest in agribusiness, industry, and renewable energy to create the jobs that young people demand. Senegal is not bankrupt. It is at a crossroads. And crossroads, in the lives of nations as in the lives of individuals, are crossed with dignity.

Cheikh Tidiane SY Al Amine, Agro-economist | Founder and CEO, BAZILA HOLDING, Member of the Executive Board of the CNP, Dakar, June 2026

Commentaires (8)

Participer à la Discussion

Règles de la communauté :

💡 Astuce : Utilisez des emojis depuis votre téléphone ou le module emoji ci-dessous. Cliquez sur GIF pour ajouter un GIF animé. Collez un lien X/Twitter, TikTok ou Instagram pour l'afficher automatiquement.